Personal loans can be a powerful financial tool when used wisely. However, understanding the options and terms can be complex. With the right information, you can make smart borrowing decisions that improve your financial future. This guide covers everything you need to know about personal loans. Learn about the different types, how to apply, the costs involved, potential risks, and smart strategies for using them.

What is a Personal Loan?

A personal loan is an unsecured installment loan, typically repaid with fixed monthly payments over a period of 1 to 7 years. You borrow a lump sum, agree on an interest rate, and follow a fixed repayment schedule. Unlike mortgages or car loans, personal loans are often unsecured, not tied to an asset like a house or vehicle.

For a breakdown of how personal loans compare with credit cards and other forms of debt, check out NerdWallet’s guide.

Types of Personal Loans

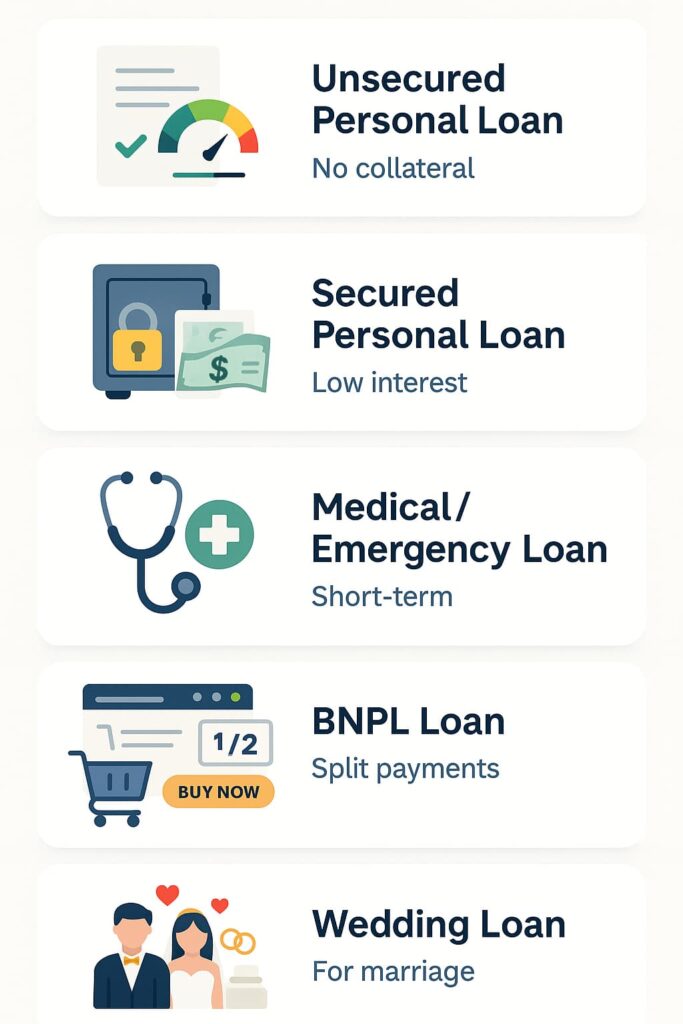

- Unsecured Personal Loans

No collateral required. Approval depends on your credit score. Interest rates are higher because the risk for lenders is greater. - Secured Personal Loans

These loans typically require collateral, such as a car or savings account. They are easier to qualify for, even with fair credit. Because the lender has some security, they often offer lower interest rates compared to unsecured loans. - Debt Consolidation Loans

These loans help combine multiple debts into one payment. They often offer a lower interest rate. This can simplify your finances but may increase the overall repayment period. - Medical or Emergency Loans

Specifically for unexpected expenses. Regulators sometimes impose interest-rate caps to protect consumers from predatory lending practices. - Buy Now, Pay Later (BNPL) Loans

These are short-term installment loans offered at checkout by e-commerce sites. While convenient, failure to repay can impact your credit. - Wedding Loans

Tailored for couples planning weddings. These loans can cover venues, attire, catering, and even honeymoons. They help spread the costs into manageable payments. - Home Improvement Loans

Used for repairs, remodeling, or upgrades. Often chosen to boost property value or fund energy-efficient upgrades.

Why Use a Personal Loan?

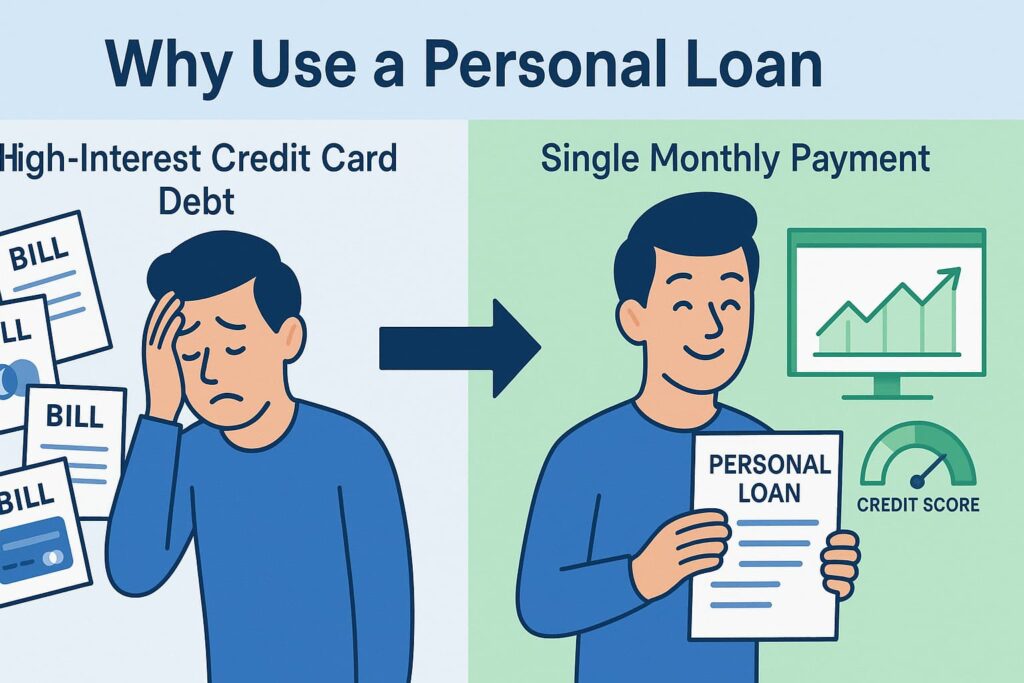

Manage High-Interest Debt

You can use a personal loan with 10% interest to pay off credit cards charging 20 to 30% interest. This strategy can save you hundreds or even thousands of dollars.

Finance Major Expenses

Use it for home improvements, wedding costs, or large life events. This is often cheaper than relying on credit cards.

Financial Flexibility

Unlike credit cards, personal loans give predictable monthly payments and no revolving credit. This allows better budgeting.

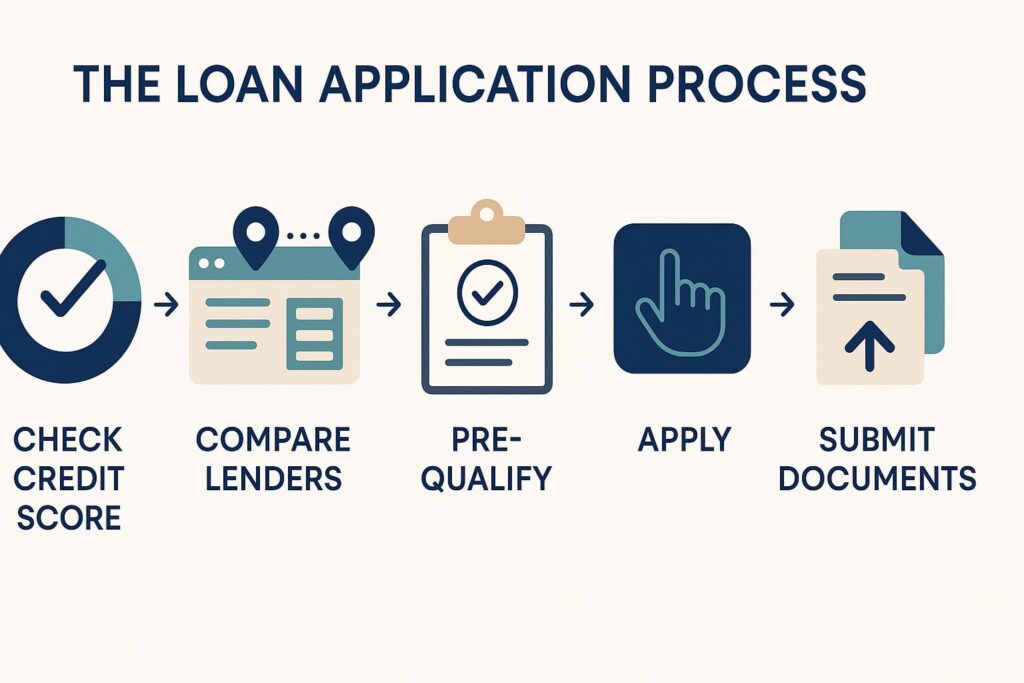

The Application Process

1. Check Your Credit Score

Lenders classify your credit score as:

- 750+ = excellent

- 700–749 = good

- 650–699 = fair

- Below 650 = poor

You can check your score for free using services like Credit Karma. Also, request your full credit report to spot any errors. You’re entitled to one free credit report each year from the three major credit bureaus. Visit the Consumer Financial Protection Bureau’s credit report guide for direct access and detailed instructions.

2. Compare Lenders

Investigate:

- Rates & APRs

- Term lengths

- Fees (origination, prepayment penalties)

- Customer reviews

Tip: Use loan comparison tools like LendingTree or Bankrate. Also, assess lender transparency, hardship policies, and mobile access, especially if you prefer managing your loan through an app.

3. Pre-Qualification

A soft credit pull helps you compare offers without hurting your credit score.

4. Apply & Submit Documents

Typically requires:

- Government-issued ID

- Recent payslips or bank statements

- Employer details or proof of business (if self-employed)

Loan Fees & Interest: What to Expect

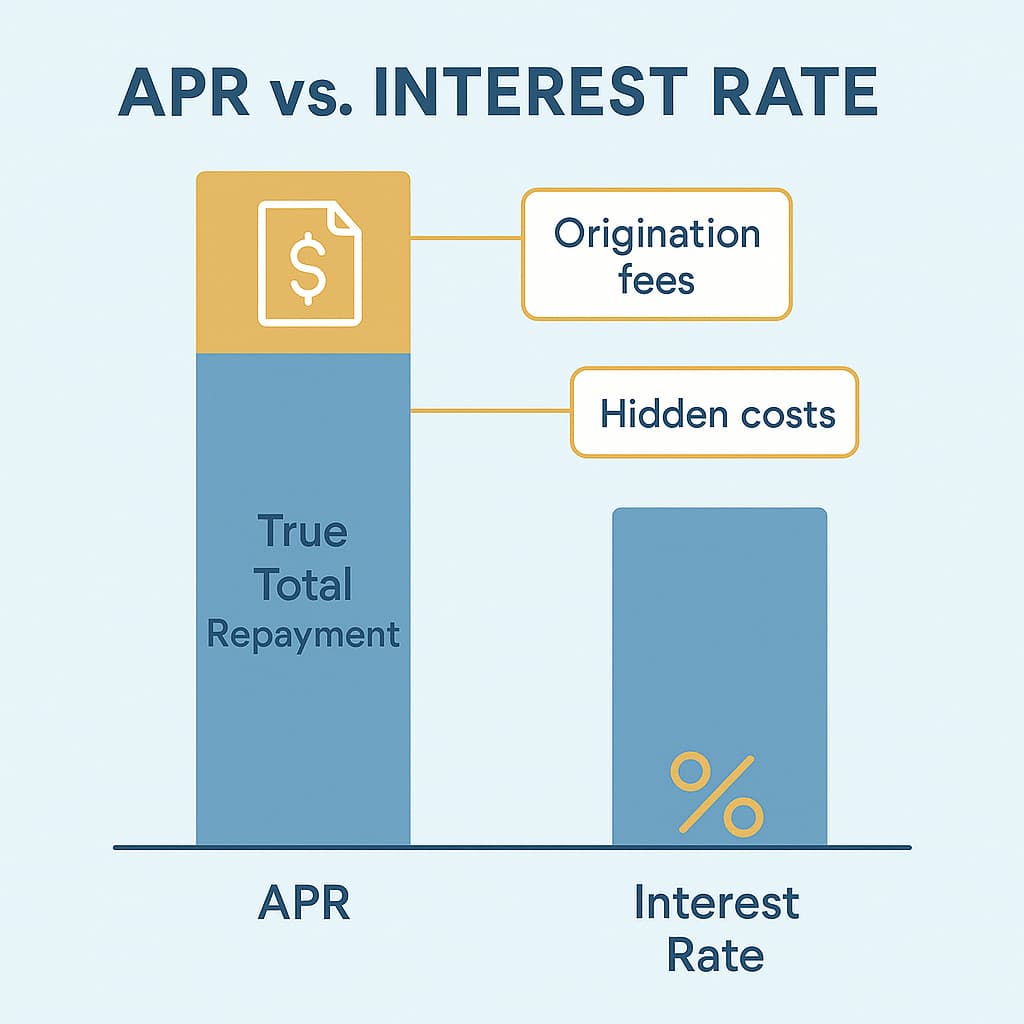

Interest Rate vs. APR

The APR (Annual Percentage Rate) includes fees and reflects your true loan cost. Always compare APR, not just interest rate.

Origination Fees

Charged at loan approval; usually 1–6% of the loan amount.

Late Payment Fees

Missing even one payment can lead to late fees and damage your credit score.

Prepayment Penalties

Some lenders penalize you for paying off your loan early. Always read the fine print.

How Personal Loans Affect Your Credit Score

Applying for a personal loan results in a hard credit inquiry, which can slightly lower your score temporarily. But once approved, timely repayments can help build your credit by improving your payment history and credit mix.

Defaulting or missing payments, however, can seriously harm your score. Keep your debt-to-income ratio in check. Too much debt can reduce your future borrowing ability.

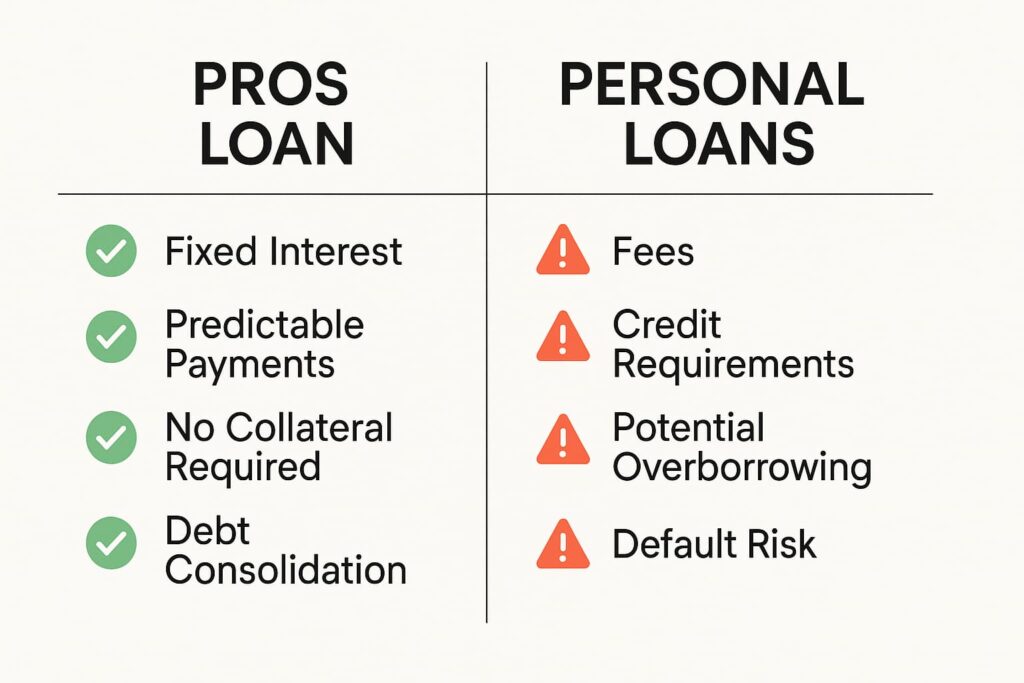

Pros & Cons of Personal Loans

Pros

- Predictable payments and term

- Can consolidate high-interest debt

- Fixed interest rate (no surprises)

- Useful for building credit if paid responsibly

Cons

- High rates for poor credit

- Fees can reduce the net amount received

- Borrowing more than necessary can lead to overspending

- Can be used irresponsibly, leading to a debt spiral

How to Choose the Right Personal Loan

Know Your Purpose

Debt consolidation needs differ from loans for travel or home renovation.

Evaluate APR, Fees, and Total Cost

Lower interest may be offset by high fees. Always calculate the total repayment amount.

Compare Loan Terms

Longer terms = lower monthly payments but more total interest.

Check Lender Reputation

Use sources like the Better Business Bureau or Trustpilot for reviews. Learn how you can recognize and prevent digital financial fraud to stay protected from predatory lenders. Scammers are even starting to use deepfake videos to impersonate lenders or financial experts. Understand how to spot visual manipulation in our visual guide on recognizing deepfakes and AI-generated videos.

Quick Checklist Before Applying for a Personal Loan

- Know your credit score

- Compare at least 3 lenders

- Understand APR vs. interest rate

- Check for prepayment or origination fees

- Calculate your monthly repayment

- Ensure the loan fits your monthly budget

Alternatives to Personal Loans

- Home Equity Line of Credit (HELOC) – Lower rates, but your home is collateral.

- Balance-transfer credit cards – 0% offers for 12–18 months, but watch for balance transfer fees.

- Peer-to-peer lending – Platforms like Prosper offer flexible lending with low rates.

- Family/friend loans – May be interest-free but could strain relationships if mismanaged.

Smart Use of Personal Loans

- Borrow only what you need.

- Automate monthly payments to avoid late fees.

- Use loans to improve your financial future, not weaken it.

- Track your payoff progress using budgeting tools or apps like YNAB or Mint.

Modern AI-driven budgeting apps can also help automate your repayment tracking and spending plans. Learn more about how AI is shaping everyday tools in our article on how artificial intelligence is becoming part of daily routines.

When to Pay Off Early (and When Not To)

Good Idea If:

- You want to save on interest

- You have extra cash beyond your emergency fund

Avoid Early Payoff If:

- It incurs penalties

- You have higher-interest debt elsewhere

- The money could be better invested for higher returns

When to Avoid Personal Loans

Avoid taking a personal loan if:

- Your income is unstable

- You lack a realistic repayment plan

- The funds would go toward non-essential spending

- You’re already struggling with existing debts

In these cases, explore alternatives or delay borrowing until your financial situation stabilizes.

FAQs

What credit score do I need?

Typically 650+ for unsecured loans; 700+ for better rates.

Can I use a personal loan to pay off credit cards?

Yes, but avoid the temptation to reuse the credit.

Should I choose secured over unsecured?

If your credit is weak and you can provide collateral safely, yes.

How many personal loans should I apply for?

Limit to 1–2 pre-qualifications to avoid harming your credit score.

Final Thoughts

Personal loans are useful for debt, big purchases, or improving finances when used wisely.

Remember to:

- Borrow based on real need

- Understand total cost and APR

- Compare multiple lenders

- Plan your repayment from Day 1

Personal loans can support your financial goals. With careful planning and responsible use, they become a smart strategy.

Leave a Reply